Christmas is fast approaching and we all appreciate the little gifts we receive from loved ones but is helping your adult child buy their first home a help or a hindrance?

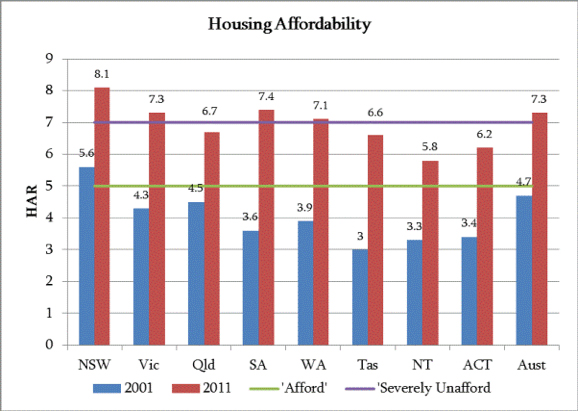

It is not difficult to understand why adult children are turning to their parents for a step up on the property ladder. In a Parliamentary report titled, “Out of reach? The Australian housing affordability challenge” (8th May 2015), there are some shocking statistics. Up until 2001 annual income grew in line with housing prices, since 2001 the growth in property values has dramatically outstripped growth in household incomes. NATSEM [National Centre for Social and Economic Modelling] data shows that house prices increased by 147 per cent compared to income growth of just 57 per cent between 2001 and 2011. In dollar terms, the median price of a house more than doubled from $169,000 to $417,500 while after tax income increased from just $36,000 to $57,000. Whereas in 2001 an average home price in Australia was 4.7 times the average income, by 2011 this had increased to 7.3 times.

This graph below (source: Master Builders Association), highlights the housing affordability issue in Australia.

The Housing Affordability Ratio is measured by dividing the median house price by the median income of the house purchaser. A ratio of 5 or less, below the green line, is considered affordable, a ratio of 7 or more, above the purple line is severely unaffordable. This horrific statistic can provide some insight as to why parents are assisting adult children fund their first home. Question is, should we be?

This can be a very difficult question to answer. Prior to gifting money to your adult child, funding their deposit or going guarantor on a loan, make sure you consider the following:

- Will you have enough money to fund your own retirement if you assist your children?

- If you go guarantor on the loan and your adult child’s circumstances change and they can no longer fund the mortgage repayments. Will you be able to meet these repayments? If not, there could be serious consequences for your own financial stability.

- Should your adult child be in a relationship and live with their partner and things turn sour resulting in a relationship break up, watch the can of worms open up! If you paid the deposit or funded the home, the law may see it as a gift and the ex-partner walks away with half or more! Alternatively, if you are guarantor on the loan: What are the financial implications with the split?

- Have you taught your adult child how to manage their finances on their own? If you are generous and assist them with their first home purchase they may not appreciate the value of a dollar. The best lesson in life when it comes to financial savings is delayed gratification. What you need to give up now to get something in the future can be a great value to instil in your child. If it is out of reach, then maybe it should never have been!

- If the bank will not loan the funds to your adult child, the risk must be high. If you guarantor the loan you take on this risk.

- Is your adult child willing to make sacrifices to invest in property? When I talk of sacrifices, I refer to their willingness to purchase in an affordable area that may be many kilometres from the city and to also manage their spending carefully.

This is not an exhaustive list but it does provide food for thought. If you do decide to assist your adult child it would be a good idea to ensure agreements are in writing and clearly understood. Life can often change course when we least expect it.

I have an adult child, still studying at University and living at home and understand the difficulty in wanting to provide for their financial future. Maybe times are changing and the reality of home ownership in Australia is now only a dream. Long term leases could pave the way for our kids into the future, so maybe you should be the one investing in another property!

Justine Thomson